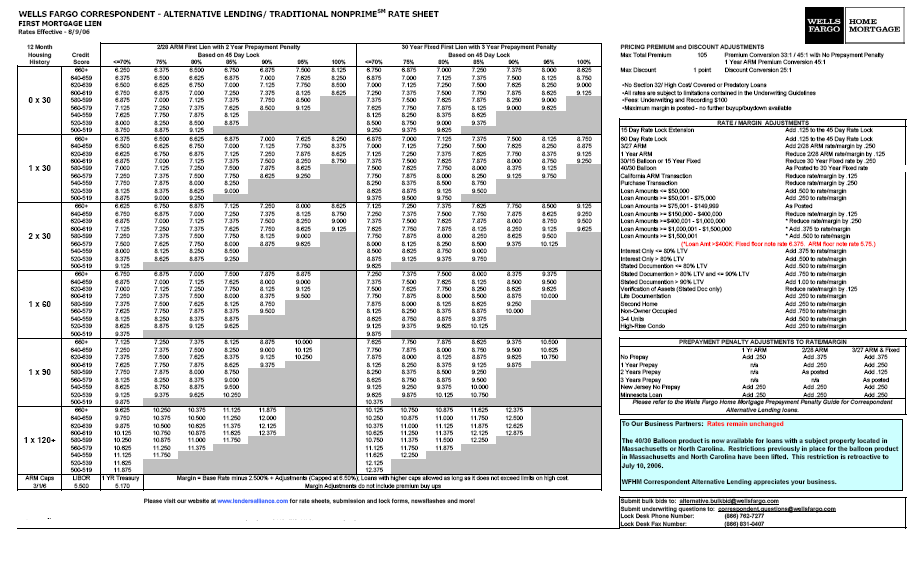

Fidelity Helps to make the Instance Resistant to the 401(k)

Fidelity only put out the quarterly study regarding account in the 17,500 401(k) arrangements it administers. The country's number one administrator and movie director away from 401(k) assets accounts that the balance within the mediocre account rose 13.5% so you can $53,900--an enjoyable dive. Up coming, inside a strange go after-upwards ability, they detailed what its experts got recognized as "secret habits that will be hindering offers for specialists during the various other lifetime amount." It reads (inadvertently, definitely) such a behavioural economist's book indictment of your own difficulties with the new 401(k) concept.

So long as the latest plans enable individuals to capture financing to possess what they imagine a lot more clicking need, or even spend money ranging from jobs, or perhaps not take part in the new arrangements before everything else, they are going to

Younger pros try not to engage. "Fewer than half (44%) away from qualified experts inside their 20s sign up for its work environment agreements today."

For as long as the brand new plans allow visitors to simply take loans to own whatever they imagine so much more pressing need, or perhaps to spend money ranging from efforts, or perhaps not take part in new preparations in the first place, might

Members of their 30s and you can forties borrow too much regarding agreements. The brand new statement notes that individuals inside age group have clicking needs due to their currency that will be nearer at hand than just later years, including creating a family group and you may obtaining a house. As a result, they have a tendency so you're able to use heavily from their 401(k)s. ". [N]very early one out of five experts (23%) inside age bracket keeps one or more outstanding finance, and more than one in ten (10.6%) initiated that loan for the past 12 months. pros in this age group including tend to be recite mortgage pages. Almost one-third (31 %) off carried on energetic professionals within age bracket just who took a beneficial loan a year ago and got one this current year."

Provided the fresh new plans enable individuals to get fund having what they consider far more pressing requires, or perhaps to spend currency ranging from jobs, or otherwise not take part in this new agreements before everything else, they will

Older experts often grab a lack of otherwise an excessive amount of financing chance. "More than a quarter (26%) away from pre-retirees often don't have any exposure to equities or hold 100 percent equities within their 401(k) bundle. Multiple inside ten (eleven.4%) pre-retired people keeps no equities within 401(k) package, a technique who's got typically led to significantly all the way down output toward a rising prices-adjusted foundation as opposed to those out of a great deal more varied profiles."

For as long as brand new arrangements enable people to simply take fund for what they imagine so much more pressing demands, or even spend money between perform, or perhaps not take part in the agreements before everything else, they will certainly

Anyone mis-go out the market When you're Fidelity did not establish it as a lives-stage-associated situation, they performed note that its plans' players had began investing a whole lot more conservatively since industry took place. Often the stock allotment from the profile averages to 75% (they toppped away at 80% at the top of the new tech stock ripple). It's now down seriously to 68%, only over the years to overlook the biggest rebound rally because the High Despair.

It is the look at the fresh new 401(k) globe (comprehend the comment regarding Financing Organization Institute to my past article and Nathan Hale's enchanting reaction), it is the business out of well-intentioned businesses and plan administrators to teach people to not make mistakes such as these. As if several hours in a room having a great whiteboard and you may cake charts do lay people focused to help you retire prosperously.

But positively, group. It is far from a lack of monetary literacy that makes a majority out-of 20-year-olds maybe not participate in a 401(k). It is human instinct online personal loans Hawai. Just how many at this decades are planning 40 years toward coming? Furthermore, whenever is 30- and you may forty-year-dated householders perhaps not probably put the quick requires of its increasing household members through to the however extremely theoretic needs of their retired selves, twenty-five or 40 years off? For 401(k) investors' tendency to rating as well conventional otherwise too aggressive at only not the right big date, while in submitted history has buyers maybe not over you to definitely?

Yes, we want a retirement deals bundle in this country one to, like the 401(k), brings together new operate out of regulators, employers and employees to help make a supply of sufficient income during the retirement. It has to be reasonable in the mans choices. For folks who give some body new freedom to place small-name means just before their long-identity discounts need, they will certainly, and they're going to wind up short of senior years currency because an effective impact. Fidelity's declaration is pretty obvious research.

Cet article vous a plû ? Partagez-le à votre équipe !

Nous utilisons des cookies afin de mesurer notre audience, évaluer la performance de nos actions de marketing et vous proposer une meilleure expérience.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Durée

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.